Institutions Aren't Moving Independently Anymore

TL;DR

- Asset issuers, banks, and exchanges have stopped operating in parallel; they've formed a pipeline where each layer depends on the others.

- Control of the infrastructure layer means control over compliance rules, fee structures, and access terms for everyone built on top of it.

- The institutions designing their own infrastructure now will set the terms; the ones adapting later will inherit them.

For the last decade, asset issuers, banks, and exchanges each worked their own corner of the digital asset problem: issuers tokenizing assets, banks building custody and settlement infrastructure, exchanges building liquidity and access. Clean separation, independent timelines, parallel development.

That model has broken.

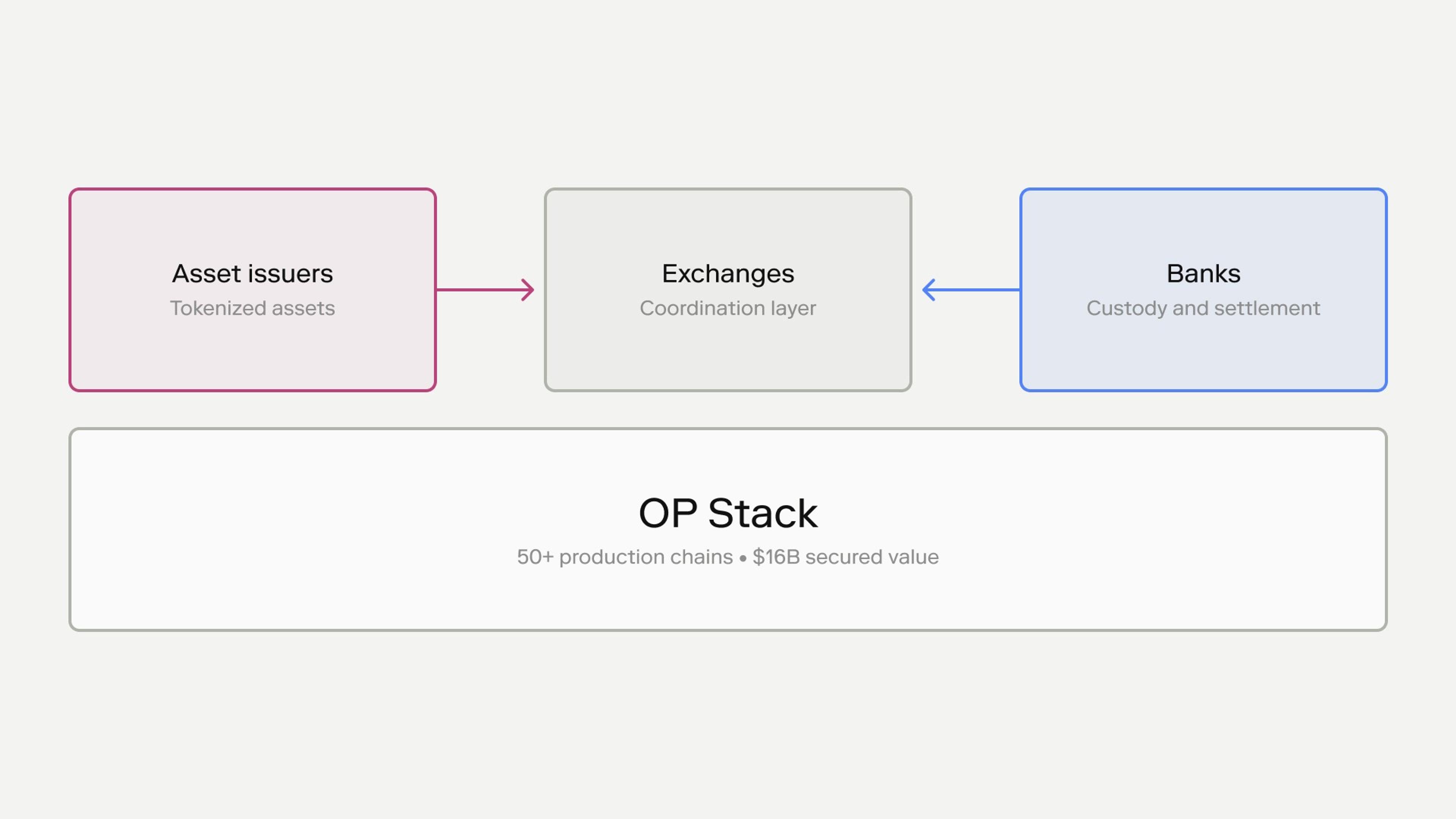

These players no longer operate independently; they've formed a pipeline. Issuers need exchanges for distribution. Banks need infrastructure that plugs into both. Exchanges are in a race to avoid being bypassed entirely. We've watched this form across 50+ production chains on the OP Stack, representing $16 billion in secured value. The system only works when the layers align, and who controls the terms of that alignment is now the actual competition.

The technology is largely available. Who defines the coordination layer is what's being decided.

Asset Issuers: The Control Problem

Tokenization has moved from concept to execution. Fidelity, WisdomTree, and BlackRock are actively bringing products onchain. Regulatory clarity has improved; the SEC's recent guidance allows issuer-led tokenization models to move forward without waiting for a counterparty to initiate.

But execution reveals a different constraint. Asset issuers are no longer asking how to tokenize. They're asking where those assets live, trade, and settle.

The answer

The answer, in practice, is distribution. Issuers are increasingly dependent on exchanges to provide it, not just for liquidity, but for compliance infrastructure, user access, and global reach. Even early implementations like BlackRock's BUIDL run through tightly controlled distribution paths rather than open systems. The issuer defines the asset; the exchange defines who gets it and on what terms.

The dependency is new, and it creates a real problem.

Controlling your Infrastructure

If your asset lives inside someone else's infrastructure, you don't control how it moves, who accesses it, or how revenue accrues. You've tokenized an asset and handed the value to someone else.

The institutions moving fastest are solving for this at the infrastructure layer: building chain environments where they define the compliance rules, access controls, and settlement logic rather than inheriting them from a third party. The OP Stack handles the underlying infrastructure (the boring, expensive part) so the institution's team is actually configuring a product instead of building a protocol.

Banks: Extension, Not Replacement

Banks are not redesigning their core systems; they're layering new capabilities on top of what already works.

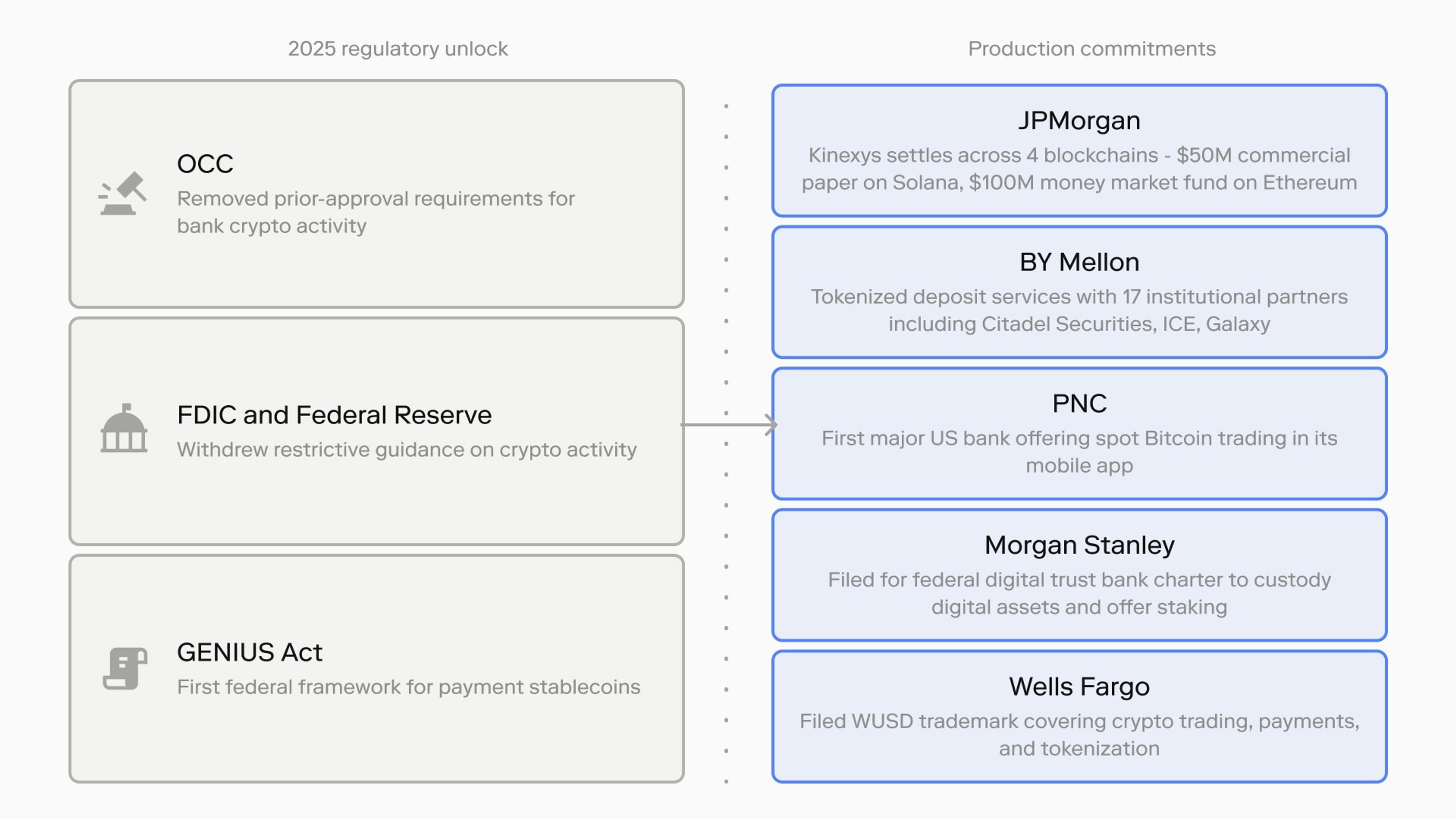

The regulatory environment shifted decisively in 2025. These changes didn't create demand; they unlocked activity that was already waiting:

These aren't pilots. They're production commitments from institutions with combined balance sheets in the tens of trillions.

The constraint is the same across all of it: banks cannot introduce new systems that increase operational or regulatory risk. Integration has to be incremental. Compliance has to be embedded from the start, not retrofitted. The infrastructure they adopt has to fit into existing systems, not replace them. Chains built on the OP Stack inherit the operational infrastructure and compliance tooling developed across 50+ production deployments, which matters specifically because banks aren't in the business of running novel infrastructure; they need the boring parts already solved.

Exchanges: The Coordination Layer

Exchanges now sit at the center of this system. Issuers rely on them for distribution. Banks rely on them for liquidity and access. Users rely on them as the primary interface.

Traditional market infrastructure is moving fast to avoid being cut out. NYSE and Nasdaq are exploring tokenized equities. DTCC is expanding its scope specifically to stay relevant as settlement logic moves onchain. The question for exchanges isn't whether to participate; it's how much of the value chain they control when they do.

The stakes are highest here, because the leverage runs in both directions. Kraken launched Ink on the OP Stack. OKX migrated X Layer to the OP Stack. Both made the same calculation: operating on shared infrastructure means inheriting shared economics; operating on infrastructure you control means defining your own.

Fee structures, compliance frameworks, product design, integration paths with banks and issuers. All of it becomes configurable instead of constrained. That difference doesn't show up in the first quarter. It compounds across every partnership, every product launch, every fee that would have gone elsewhere.

Where the infrastructure is owned is where the decisions get made.

The System Only Works When the Infrastructure Aligns

The pattern is consistent across all three. Each is moving toward infrastructure it can control, because control is what lets it serve the others without ceding economics to them.

Infrastructure that extracts value from every layer creates friction. Infrastructure that aligns incentives across layers scales. That sounds like a principle but it's really just the math: every toll collected by a neutral platform is revenue that should have gone to the operator.

The institutions moving first are designing for this specifically: customizable execution environments, compliance frameworks defined at the protocol level, revenue models that belong to the operator. That's the structure forming across the deals already in production.

The ones adapting later will be adapting to terms they didn't write.

Authored by

Optimism